Housing prices in Bulgaria over the last 100 years: historical review and analysis

Author: imi.bg | Uploaded before 9 months

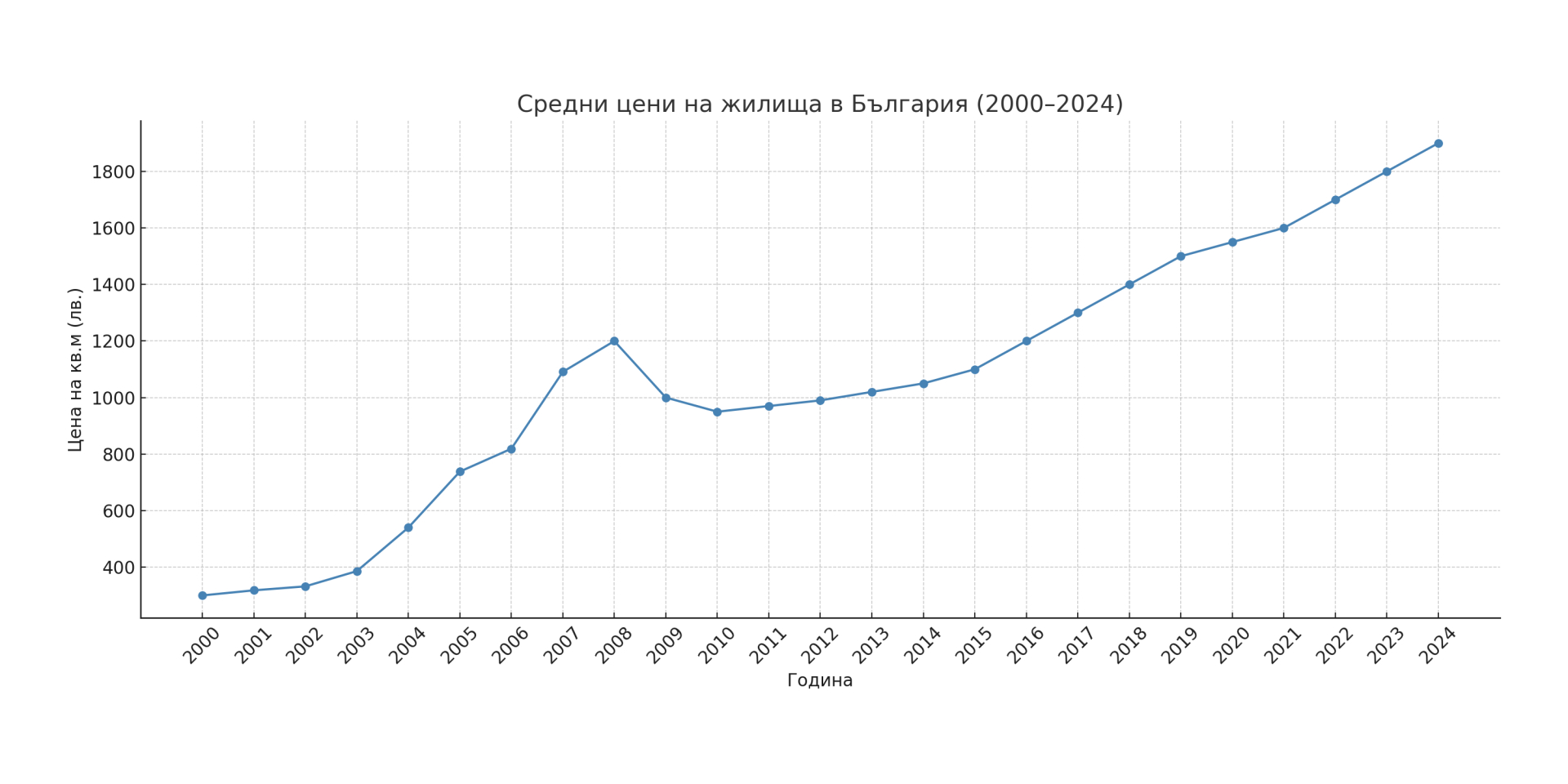

<p data-start="90" data-end="315"><em data-start="132" data-end="314">House Price Index in Bulgaria (2010 = 100). The boom of the 2000s was followed by a decline after 2008, and in the last decade prices have risen again to record levels.</em></p><p data-start="317" data-end="921"> Over the course of a century, the Bulgarian housing market has undergone dramatic upheavals – from the modest market at the beginning of the 20th century, through decades of state regulation and shortages, to the modern cycles of sharp rises, falls and new peaks. Housing prices in Bulgaria have been strongly influenced by historical events and economic regimes. Examining this period provides a valuable perspective for the professional audience: investors and economists can trace how wars, political changes, inflation, urbanization and global processes have shaped the demand, supply and affordability of housing.</p><h2 data-start="923" data-end="972"> Early 20th century: a modest market and an agrarian society</h2><p data-start="974" data-end="1742"> At the beginning of the 20th century, Bulgaria was a predominantly agrarian country with a small urban population and an underdeveloped housing market. Most people lived in modest living conditions and modern home ownership was rare. Before World War II, nearly 80% of Bulgarians lived in simple two-room houses made of adobe (unbaked bricks) in rural areas. Cities were still small, and housing there was limited and available mainly to the wealthier. The mass population lived in overcrowded one- or two-room country houses, often in multi-member households. In these conditions, the concept of “market price” of housing was relative – properties rarely changed hands and were more likely to be inherited or built independently by families.</p><p data-start="1744" data-end="2511"> The economic turmoil between the two world wars further limited the development of the real estate market. The Great Depression of the 1930s also affected Bulgaria - incomes fell, which limited the possibility of investing in housing. The state made attempts to improve the living conditions of workers in the cities by building the so-called "workers' housing", but the scale was small compared to the needs. At the end of the 1930s, the housing infrastructure remained backward: most rural homes lacked basic amenities (over half did not have a water well or an indoor toilet). During this period, the value of real estate grew slowly and mainly reflected the value of the land and outbuildings, rather than the housing itself.</p><p data-start="2513" data-end="2935"> The Second World War (1939–1945) brought new devastation. Although Bulgaria was not a battlefield in the full sense, the bombings of 1943–1944 caused damage to cities such as Sofia. After the war, the country faced a housing shortage and the need for reconstruction. It was at this point that the political system changed dramatically – a pro-Soviet regime was established, which would transform not only the economy but also the housing sector.</p><h2 data-start="2937" data-end="3013"> Socialism (1945–1989): state control, mass construction, and shortages</h2><p data-start="3015" data-end="3826"> After 1945, the Bulgarian state assumed a centralized role in the economy and housing planning. Private initiative in construction was practically replaced by planned development. Already in the late 1940s and early 1950s, many private properties (especially townhouses and buildings) were nationalized. Legislation limited the right to private ownership of housing - a family was allowed to own only one main residence and one villa (holiday) building. The state set fixed property prices and rents, which were significantly lower than market levels. Buying and selling were highly regulated: citizens could buy a home only with special permission and often had to wait for years on waiting lists.</p><p data-start="3828" data-end="5057"> As urbanization accelerated – especially in the 1960s with industrialization – the government began large-scale housing construction to accommodate the growing urban population. Huge neighborhoods of panel blocks (mass-produced factory-made reinforced concrete elements) and large-area formwork (EPK) buildings appeared. By 1989, over 60% of the country’s population already lived in these government-built housing complexes. State-owned enterprises and institutions allocated apartments to their workers according to strictly defined criteria – such as marital status and length of service. The price of newly built apartments is subsidized by the state and fixed – a three-room panel apartment in the late 80s officially costs about 20,000 leva, a two-room apartment – ~14,000 leva, a one-room apartment – about 9,000 leva. These prices are affordable compared to the salaries of the time (for example, the average salary was about 200 leva), but practically few people can get a home right away. Usually, they wait in line or rely on a state housing loan with a low interest rate from DSK (the state savings bank).</p><p data-start="5059" data-end="5810"> An alternative <strong data-start="5072" data-end="5087">unofficial</strong> market does exist: if someone wants to acquire a home without waiting, they have to pay a significantly higher “black” price. According to unofficial data, in the mid-1980s, a three-room apartment in the center of Sofia was sold illegally for 40–50 thousand leva – more than double its state value. These amounts are equivalent to dozens of average annual salaries and reflect the huge discrepancy between demand and supply. The rental market is also controlled – rents in the late 1980s were symbolic (for example, about 90 leva per month for a room and 280 leva for an entire three-room apartment), but there are practically no vacant apartments outside those allocated by the state.</p><p data-start="5812" data-end="6444"> State control during socialism achieved a significant increase in the housing stock – especially in cities – but the shortage was not overcome. Many young families lived with their parents or in small studios while they waited for better housing. Housing was <strong data-start="6060" data-end="6073">undervalued</strong> in an economic sense, as fixed prices did not reflect real utility and demand. By the end of the 1980s, latent potential for price increases had accumulated: properties were actually more valuable than official prices indicated, and housing density was high. All this created the conditions for significant changes when market mechanisms returned.</p><h2 data-start="6446" data-end="6517"> The transition in the 1990s: liberalization, hyperinflation and the beginning of the market</h2><p data-start="6519" data-end="7385"> With the political changes of late 1989, the housing sector entered a period of chaotic transformation. Centralized distribution was abolished, and property ownership was liberalized. The state quickly transferred a large part of the housing stock into the hands of citizens: tenants were given the right to purchase the state-owned apartments in which they lived, often at symbolic prices. Thus, in the early 1990s, Bulgaria moved to one of the highest shares of private housing ownership in Europe. At the same time, restitution was underway - properties taken away by the previous regime (plots, houses) were returned to the former owners or their heirs. This led to a one-time increase in supply on the market: many restituted urban properties were put up for sale, as their new owners often did not have the opportunity or desire to manage them.</p><p data-start="7387" data-end="8701"> The first years of a market economy, however, were marked by economic crisis, high inflation, and uncertainty, which suppressed both construction and transactions. In the early 1990s, apartment prices were extremely low, measured in hard currency – according to brokers, deals were concluded at prices <strong data-start="7694" data-end="7726">of around 2–3 euros/sq m</strong> for housing in the countryside, and even in Sofia, panel houses were offered for around $100/sq m in 1990 (in dollar terms). These values reflect the combination of reduced demand (the population is becoming poorer, unemployment is growing) and recently increased supply (privatized and restituted properties). In the middle of the decade, instability reached a peak – in 1996–1997, the country experienced hyperinflation, in which the prices of all goods, including properties, soared in nominal terms, and the lev depreciated dramatically. Interest rates then exceeded 1000% per annum, which practically stopped all bank lending for home purchases. The few transactions were carried out in cash (often in US dollars) and at greatly reduced real prices - for holders of a stable currency, these months were an opportunity to acquire properties for small sums.</p><p data-start="8703" data-end="9558"> After the introduction of a currency board in 1997 and the stabilization of the lev, the economic environment gradually improved. Macroeconomic reforms tamed inflation to single-digit levels, confidence was restored, and from the end of the 1990s a slow rise in the housing market began. Mass privatization ended, hyperinflation was brought under control, and the country's political orientation towards the West (candidateship for NATO and the EU) made Bulgaria more attractive for investment. However, the market is still in its infancy: incomes are low, mortgage lending is still in its infancy, and construction companies are operating with limited funds. Prices at the end of the decade remained far below the levels of the socialist era, if translated into world currency. But the foundations of a new, market-oriented housing sector have already been laid.</p><h2 data-start="9560" data-end="9637"> The free market boom (2000–2008): credit, investment and double-digit growth</h2><p data-start="9639" data-end="10338"> The beginning of the 21st century marks the first major upswing in the Bulgarian housing market under market conditions. Stable economic growth (over 4% per year in the period 2001–2005) increases household incomes and confidence. Inflation is relatively low, the currency board guarantees a predictable exchange rate, and the banking sector – now largely owned by foreign banks – begins to actively grant mortgage loans. Interest rates, although high by today's standards, fall significantly compared to the 1990s, and for the first time the middle class gains access to housing loans. Latent demand appears: many families who postponed purchases in the 1990s are now becoming more active.</p><p data-start="10340" data-end="11079"> In parallel, Bulgaria has been on the radar of international property investors. Around 2003–2004, foreign buyers – initially from the UK and Ireland, later from Russia and other countries – began to acquire real estate in Bulgaria. Low prices compared to Western Europe and the expected accession to the EU make Bulgarian holiday apartments on the Black Sea coast and in ski resorts extremely attractive. Also, since 2007, EU citizens can freely buy land in Bulgaria, removing the last obstacles to foreign investment in housing. Foreign interest has added fuel to an already heating market.</p><p data-start="11081" data-end="11974"> The result was an unprecedented construction and price boom. Between 2003 and 2008, housing prices rose at double-digit rates every year. Average property values in the country increased nominally more than threefold between 2000 and 2008. In Sofia and the larger cities, the price increase was even steeper, as demand was most concentrated there. Construction activity reached record levels – thousands of new apartments and houses were built annually. However, supply was struggling to keep up with the rapid demand. In the midst of this boom, some analysts warned of overheating and the formation of a property “bubble”. In 2007, Bulgaria became a member of the EU, which further increased optimism. The mortgage market also exploded – banks massively extended loans with minimal requirements, with credit expansion supporting price growth.</p><p data-start="11976" data-end="13414"> By 2008, a historic peak had been reached: housing in Bulgaria had never been more expensive in recent history up to that point. But global events soon reversed the trend. The global financial crisis of 2008–2009 quickly spread to the Bulgarian property market. Foreign buyers withdrew, credit flow dried up sharply, and the economy fell into recession. The boom ended dramatically – after 2008, housing prices in Bulgaria fell by about <strong data-start="12419" data-end="12458">30–40% from their peak values</strong> . There was a period of several quarters of practically frozen transactions – sellers were unwilling to lower prices, and buyers were waiting for better offers. Eventually, the market found a new equilibrium at significantly lower levels. The decline was widespread: resort and vacation properties were the hardest hit (where prices sometimes fell by half from their peak), while in the big cities the correction was more moderate but still significant. By the end of 2010, average house prices in the country had returned to roughly 2005–2006 levels, erasing the years of euphoric growth. In real terms (adjusted for inflation), the cumulative growth for the decade 2000–2010 turns out to be about +69%, far more modest than the nominal, but still positive – an indicator that despite the collapse, homes are retaining some of their acquired value.</p><h2 data-start="13416" data-end="13496"> Recovery and new upswing (2010–2020): second cycle of growth at low interest rates</h2><p data-start="13498" data-end="14199"> After the bottom in the period 2010–2012, the real estate market in Bulgaria is gradually emerging from stagnation. The economy is stabilizing again – after 2014, a new period of growth begins, albeit more moderate. Macro factors play a key role: <strong data-start="13731" data-end="13753">interest rates</strong> are reaching their lowest levels in recent history, and bank liquidity is high. As a member of the EU with a currency board, Bulgaria is indirectly influenced by the policy of the European Central Bank. In the second half of the 2010s, mortgage interest rates in our country fell to 3–4%, and subsequently even below 3% – some of the lowest in the entire EU. This significantly increased the accessibility of housing loans and stimulated new demand.</p><p data-start="14201" data-end="15103"> Since around 2014, <strong data-start="14232" data-end="14257">a gradual increase</strong> in property prices began, which gained momentum every year. The market entered a <strong data-start="14368" data-end="14392">second upward cycle</strong> . Initially, price growth was smooth (5–7% per year), supported by a real increase in income and improving employment. The presence of accumulated savings (household deposits in the banking system were growing), combined with the low profitability of alternative investments, directed many people back to real estate as a safe asset. A shortage of supply also began to appear for some segments: in the years after the crisis, construction was severely curtailed, which led to limited new supply of housing on the market. Thus, around 2016–2017, the trend was already clearly visible in large cities - available quality properties were being bought up quickly, and their prices were slowly exceeding pre-crisis levels.</p><p data-start="15105" data-end="15949"> The recovery was particularly strong in Sofia, where the concentration of economic opportunities attracted buyers from all over the country. By 2018, housing prices in the capital exceeded the peak of 2008 and continued to rise. The picture was similar in Plovdiv, Varna, Burgas - although the levels there remained slightly lower than in Sofia, the growth rates were double-digit for several consecutive years. On average for the country in the period 2014–2019, housing prices increased by about 7–10% per year. This second upswing was more balanced and prolonged than the boom in the 2000s. The element of mass euphoria and speculative foreign purchases was missing - the market was driven mainly by domestic demand and the improved economic environment (higher wages, record low unemployment around 2018–2019).</p><p data-start="15951" data-end="16612"> <strong data-start="15969" data-end="15996">Limited supply</strong> was also a factor: despite the boom, the number of new homes built grew more slowly than demand. Developers were more cautious after the 2008 experience, and they were also facing labor shortages and rising costs. This led to a situation in which demand outpaced supply – a classic recipe for rising prices. Thus, by 2019, the property market had effectively reached a new peak: deals were being actively concluded, prices in major cities reached historic highs, but growth still seemed to be supported by fundamental factors, not excessive speculation.</p><h2 data-start="16614" data-end="16669"> Recent years: the pandemic and beyond (2020–2025)</h2><p data-start="16671" data-end="17577"> The beginning of 2020 brought an unexpected shock in the form of the COVID-19 pandemic. The initial effect on the housing market was <strong data-start="16798" data-end="16819">a short freeze</strong> – during the lockdown, many transactions were postponed, inspections stopped, and uncertainty led some sellers to temporarily lower their offers. However, expectations of a drop in prices did not materialize; on the contrary, as in many countries around the world, so too in Bulgaria, the housing market showed surprising resilience and even acceleration after the first pandemic waves. Several factors contributed to this: historically low interest rates on loans (which remained low in 2020–2021), accumulated savings of a part of the population, and a change in preferences for more spacious housing (many people working from home decided to look for larger apartments or houses with a yard). Government incentives and a moratorium on loan payments also softened the blow for households.</p><p data-start="17579" data-end="18485"> Already in the second half of 2020, the market became more active and prices started to rise. In 2021 and 2022, this trend accelerated significantly – housing prices increased at double-digit rates on an annual basis. According to Eurostat data, Bulgaria was among the leaders in the EU in terms of housing price growth in 2022, and in the third quarter of 2024 it even recorded the highest quarterly price increase in the Union. Specifically, by the second quarter of 2024, the prices of newly built homes in our country increased by <strong data-start="18154" data-end="18179">15.6% on an annual basis</strong> – a jump compared to ~9% annually earlier, and one of the highest increases observed in recent history. This led prices to another historical peak. Properties that a decade ago were selling for $50–60 thousand now often exceed €100 thousand and more, especially in Sofia.</p><p data-start="18487" data-end="19488"> Of course, these rates have significantly outpaced income growth, which has raised the question of <strong data-start="18587" data-end="18615">housing affordability</strong> . Indicators such as price-to-income and price-to-rent ratios have deteriorated – housing has become more unaffordable for the average buyer than it was a few years ago. Some households have shifted their focus to buying in more remote locations or have remained in the rental market. Industry data shows that by the end of 2024, about 20% of potential buyers have <strong data-start="18969" data-end="18994">given up or postponed</strong> a purchase due to excessively high prices and more difficult financing. Mortgage interest rates have been gradually rising since the second half of 2022 (after the ECB raised its key interest rates in response to inflation). Although the increase is moderate, this has further cooled the most fervent enthusiasm. The market has entered a phase of calm – price increases by 2023–2024 slowed down from the peak in 2022, and the number of deals decreased slightly.</p><p data-start="19490" data-end="20268"> However, one should not be dramatic – there are still no signs of a sharp decline. Rather, the Bulgarian housing market in early 2025 is <strong data-start="19621" data-end="19636">rebalancing</strong> after the rapid rise: sellers are becoming more willing to make concessions, and buyers are becoming more careful in their assessment. From a fundamental point of view, some of the pressure on demand remains: the labor market is stable, incomes (although eaten up by inflation in 2022) are still growing nominally, and housing continues to be perceived as a protection against currency depreciation. In addition, the supply is not unlimited – despite the construction boom of recent years, <strong data-start="20086" data-end="20155">the supply of quality housing in large cities is limited</strong> and many of the newly built buildings are still being sold “on the green”. All this protects prices from sharp declines.</p><h2 data-start="20270" data-end="20316"> Regional differences and demand dynamics</h2><p data-start="20318" data-end="20988"> One of the characteristic features of the housing market in Bulgaria is its strong <strong data-start="20391" data-end="20417">regional segmentation</strong> . Price trends and levels in Sofia and several large cities differ significantly from those in smaller towns and rural areas. During the 100-year period under consideration, intensive <strong data-start="20610" data-end="20625">urbanization</strong> took place: the population moved en masse from villages to cities. If at the beginning of the 20th century the vast majority lived in rural communities, by the end of the century over 2/3 of the population was urban. This process was reflected in housing demand - large cities (first of all the capital Sofia) constantly experienced a shortage of housing, while in many villages houses gradually remained empty.</p><p data-start="20990" data-end="21526"> During the socialist period, the state tried to distribute industry and population relatively evenly, building housing complexes in smaller cities as well. However, after 1989, the trend of concentration accelerated: Sofia, Plovdiv, Varna, Burgas attracted the most investments, jobs and, accordingly, people. Prices in these centers increased manifold, while in parts of Northwestern and Central Northern Bulgaria (regions with a population migrating to the capital or abroad) properties lost value or remained illiquid.</p><p data-start="21528" data-end="22376"> To illustrate the differences: <strong data-start="21557" data-end="21568">in Sofia,</strong> average prices are unprecedented – for 2015–2025, housing in the capital has increased in price threefold (from ~715 euros/sq m to ~2200 euros/sq m on average). In other large cities, the increase is also significant – in Varna, for the same period, the price rose from ~700 to ~1550 euros/sq m, in Plovdiv – from ~550 to ~1390 euros/sq m. That is, in 10 years, the values are more than twice as high in large urban centers. Conversely, in smaller cities (regional centers with a decreasing population) and especially in villages, prices have either increased minimally or have even fallen against the backdrop of depopulation. For example, in some small towns in the Northwest, houses can still be found for 10–15 thousand euros – an amount for which one cannot even buy a garage in Sofia.</p><p data-start="22378" data-end="23458"> <strong data-start="22378" data-end="22430">The gap in price levels between the core and the periphery</strong> has been widening over the years. This is a direct consequence of demographic and economic trends. As of 2021, Bulgaria’s population is under 7 million (a decline of nearly 2 million people compared to 1989), but this decline is not evenly distributed – Sofia maintains its population of around 1.3 million, while many smaller cities have lost 20–30% of their residents over several decades. In the villages, the picture is even more worrying: there are dozens of almost depopulated villages dotted with empty houses. According to the 2011 census, there were around <strong data-start="22954" data-end="23000">1.2 million uninhabited or vacant homes</strong> nationwide, which is over 31% of all homes in the country. In rural areas, almost 43% of the housing stock is empty, while in cities around 25% is vacant. This paradoxical situation – a lot of vacant housing alongside a shortage in other segments – is explained by the geographical distribution: empty homes are mostly where there are no jobs and people, and there is a shortage where people flock.</p><p data-start="23460" data-end="24387"> In Sofia, for example, the housing stock even exceeds the number of households, but the market remains expensive due to the concentration of high incomes, smaller households (more housing is sought after due to the collapse of large households into single-family homes) and investment demand. While in the deserted regions, even the abundance of vacant houses cannot revive prices, because there are no buyers. <strong data-start="23831" data-end="23859">Urbanization processes</strong> also have another effect: the desire for large cities makes it more expensive not only for housing in them, but also for the peripheral areas around them. A typical example is the expansion of Sofia towards the surrounding villages - there the prices of land and houses also jumped, practically turning them into suburbs. Local "hot spots" have also emerged along the Black Sea coast - cities such as Nessebar, Pomorie, Balchik experienced a boom due to holiday construction for foreigners, followed by stagnation after 2009 and now a certain revival with a new type of buyers.</p><h2 data-start="24389" data-end="24433"> Impact of policies, finance and investments</h2><p data-start="24435" data-end="24768"> The housing market does not exist in a vacuum – it is closely linked to government policies, the banking sector and foreign investments. During the period under review, the role of the state underwent a complete reversal: from a central planning regulator during socialism, to a market arbiter and regulator in the years of transition and EU membership.</p><p data-start="24770" data-end="25862"> <strong data-start="24770" data-end="24800">State housing policy:</strong> After 1989, the state largely withdrew from direct housing construction. Social housing (municipal apartments for vulnerable groups) today accounts for less than 3% of the total housing stock – a legacy of the mass privatization of municipal housing in the 1990s. This means that almost all supply depends on private investment and market mechanisms. Government interventions are mainly indirect – through spatial planning laws, building regulations, tax policy, etc. It should be noted that the tax burden on property in Bulgaria remains low (property tax is a small percentage of the value), which historically incentivizes the ownership of multiple properties and <strong data-start="25526" data-end="25559">the non-sale of empty homes</strong> . This results in a phenomenon: people keep empty apartments (inherited or purchased for investment purposes) because the costs of doing so are low and the hope of appreciation is high. The lack of effective policies against speculative vacant housing contributes to imbalances between demand and supply.</p><p data-start="25864" data-end="27198"> Another area of state intervention is the regulation of the banking sector and credit. <strong data-start="25942" data-end="25978">Banks and mortgage lending</strong> are a key factor in prices. By the mid-2000s, the banking system, now stabilized and privatized, was aggressively expanding housing lending. After the 2008 crisis, regulations tightened – more conservative requirements for borrowers and higher capital buffers for banks were introduced. The Bulgarian National Bank closely monitors the mortgage market and periodically issues recommendations (e.g. to limit loans with a high loan-to-value ratio). However, competition between banks, especially in the recent years of negative interest rates in the EU, led to record low mortgage rates in our country, as we mentioned. This, combined with rising incomes, improved the housing affordability indicator in 2015–2019 – the monthly payment on a typical mortgage loan constituted a smaller share of the salary than before. But in 2022–2023, the trend is reversing – rising interest rates, albeit gradually, together with rapid price growth, mean that affordability is again declining. In response, some banks and government institutions are discussing programs to facilitate young families (for example, guarantee mechanisms for mortgages with small initial capital contributions), but at this stage this is not a widespread practice.</p><p data-start="27200" data-end="28537"> <strong data-start="27200" data-end="27229">Foreign investment</strong> also has a significant impact, especially in the period of preparation for the EU and shortly after entry in 2007. The most direct impact was the participation of foreign individuals in the market – for example, British buyers, who massively acquired country houses and holiday apartments around 2004–2008. There was also corporate investment: foreign investors financed the construction of entire complexes (especially at the seaside and mountain resorts), expecting to sell them to European buyers. Some of these investments disappeared after the global crisis – some projects remained unfinished. In recent years, foreigners have been present again, but with a smaller share and their profile is different (more individual buyers from the EU, families from Russia and Ukraine looking for a second home, and even a small number of digital nomads, attracted by the low cost of living). EU policies on the free movement of capital and people facilitate these flows: after 2012, there is no longer even a restriction on foreigners buying land in our country, which has removed the last barrier. Overall, foreign investment has added volatility – accelerating growth in good times, but also intensifying declines in bad ones (an example is the Black Sea region, where the withdrawal of British buyers after 2008 led to a collapse in local prices).</p><p data-start="28539" data-end="29644"> Finally, we should also mention <strong data-start="28568" data-end="28582">inflation</strong> as a macrophone. Bulgaria has experienced various inflationary regimes – from the deflationary 1930s, through socialist hidden inflation (controlled prices, but deficits), to the hyperinflation of the 1990s and relatively stable prices under a currency board. Inflation erodes the real value of money and traditionally directs people to invest in real assets such as real estate. In the 1990s, it was the fear of devaluation of savings that pushed many to buy dollars or gold, but also real estate, as a safer “reserve”. Later, in the mid-2010s, when inflation was low (even negative in some years), this motive was absent. In 2022, however, consumer inflation rose sharply (over 14% on average annually), and this again played a role – many citizens preferred to invest their money in housing to protect it from devaluation. Thus, the inflation wave, combined with cheap credit, became one of the catalysts of the latest price spike. The subsequent tightening of monetary policy (raising interest rates) aims to cool down these overheated markets.</p><h2 data-start="29646" data-end="29690"> Prospects and expectations for the housing market</h2><p data-start="29692" data-end="29923"> Looking ahead, the question arises: where will the Bulgarian housing market go after everything it has experienced over the past 100 years? Of course, accurate predictions are difficult, but several key factors and trends can be outlined: </p><ul data-start="29925" data-end="34637"><li data-start="29925" data-end="30705"><p data-start="29927" data-end="30705"> <strong data-start="29927" data-end="29956">Demographics and urbanization:</strong> Bulgaria’s population continues to decline and age. This should in principle reduce the demand for housing on a national scale. However, internal migration and changes in household structure mitigate the effect – people will continue to cluster in economically active centers. So there will be <strong data-start="30270" data-end="30289">an oversupply</strong> in depopulating areas (where more housing will be vacant) and <strong data-start="30350" data-end="30362">a shortage</strong> in attractive cities. Policy can intervene by providing incentives for the development of medium-sized cities, but this is a long-term task. In the coming years, we will probably continue to see stratification: a high and stable price level in Sofia and several large cities, moderate prices in secondary cities and symbolic property values in the periphery. </p></li><li data-start="30707" data-end="31363"><p data-start="30709" data-end="31363"> <strong data-start="30709" data-end="30748">Economic convergence and incomes:</strong> If the Bulgarian economy continues to catch up with the European average, incomes will rise, allowing housing prices to also rise in the long term (without deteriorating affordability). It is important that the price/income ratio does not go beyond reasonable limits. It is already strained at the moment – for example, the ratio of housing prices in Sofia to the average annual salary is among the highest in Europe. If incomes do not catch up with prices, the market will hit a natural ceiling – buyers simply will not be able to afford more. We may see <strong data-start="31305" data-end="31326">a slowdown in price growth</strong> as incomes catch up. </p></li><li data-start="31365" data-end="32421"><p data-start="31367" data-end="32421"> <strong data-start="31367" data-end="31399">Interest rate policy and the eurozone:</strong> We are entering an era of higher interest rates globally, after a decade of cheap credit. If interest rates remain higher, this will severely limit speculative price inflation – access to credit becomes more expensive, and demand – more moderate. Bulgaria is aiming to enter the eurozone in the coming years. Some observers suggest that adopting the euro could temporarily increase property prices (as they have observed in other countries, where with the elimination of currency risk and the fall in interest rates, property prices increase). In our case, however, interest rates are already fixed to the euro through the board, so the effect may be less pronounced. It is more likely that <strong data-start="32096" data-end="32133">the possible entry into the eurozone</strong> will have a psychological effect – foreign investors, funds or citizens of richer countries would view Bulgarian properties as safer assets, once the country is in the eurozone. This could increase external demand, especially for prime properties, and support prices in the high-end segment. </p></li><li data-start="32423" data-end="33617"><p data-start="32425" data-end="33617"> <strong data-start="32425" data-end="32469">Condition of the existing housing stock:</strong> The issue of aging buildings should not be underestimated. A huge part of Bulgarian urban housing is in panels and old brick cooperatives from the 1960s, 1970s and 1980s. These buildings are approaching the end of their design life. In the next 10–20 years, it will be critical to invest in their strengthening, renovation or replacement with new construction. This creates both risks and opportunities. If measures are not taken, the quality of the housing stock will deteriorate and this may lower the prices of the oldest and depreciated properties (who will pay a high price for an apartment in a block that is dangerous or non-functional?). On the other hand, national renovation programs (such as the energy efficiency program launched in 2015) can increase the value of renovated old blocks and extend their life. Also, the need to replace aging buildings could stimulate <strong data-start="33338" data-end="33367">a new construction cycle</strong> – for example, demolishing old panel houses and erecting modern buildings in their place. This would activate the market and change the appearance of entire neighborhoods, but requires serious investments and good coordination between owners, municipalities and construction companies. </p></li><li data-start="33619" data-end="34637"><p data-start="33621" data-end="34637"> <strong data-start="33621" data-end="33657">Political and regulatory environment:</strong> In the future, government action will still be important. One possible direction is to introduce stricter measures against speculation – for example, higher taxes on second and third homes, or incentives for selling/renting out empty properties. Another is to encourage <strong data-start="33917" data-end="33935">the rental sector</strong> – Bulgaria is currently a country of homeowners (over 80% of households own their own homes), but this may gradually change if prices remain high and people seek flexibility. The development of institutional investors in residential rentals (such as those in Western Europe – funds that own and rent out thousands of apartments) could bring liquidity and professionalism to the rental market, although such a trend is still in its infancy. Government decisions in the field of regional development – infrastructure projects, economic growth zones – will also have an impact: for example, a new factory or university in a city can reverse migration flows and revitalize the local housing market.</p></li></ul><p data-start="34639" data-end="35518"> In summary, the housing market in Bulgaria is likely to remain <strong data-start="34706" data-end="34746">cyclical, heterogeneous and sensitive</strong> to external and internal factors. The history of the last 100 years teaches us that periods of boom inevitably alternate with corrections, and the value of real estate broadly reflects the state of the economy and society. From a poor agrarian beginning, through a command economy with fixed prices, to a globalized market – Bulgarian housing prices have come a long way. Today they are measured in thousands of euros per square meter in Sofia – a change that was difficult to imagine for our ancestors. But despite the overall upswing in nominal terms, challenges remain: to achieve a balance in which housing is both attractive for investment and affordable for the population; to ensure that supply meets demand where it is needed; and to ensure that the housing stock is of high quality and sustainable.</p><p data-start="35520" data-end="36391"> For investors and economists, the lesson is that real estate in Bulgaria follows the logic of <strong data-start="35624" data-end="35660">economic cycles and structures</strong> : fundamental factors such as demographics, incomes and interest rates ultimately determine the direction, although in the short term emotions and expectations can deviate it. The prospects for the housing market will depend on how well the country manages to retain and attract people, increase their well-being and integrate its market with global financial flows without losing control. If these conditions are favorable, history suggests that in the long term, housing prices will continue their upward trend – but probably at a more moderate pace and subject to temporary corrections. After a century of dramatic changes, the Bulgarian housing market is reaching a maturity in which past experience can serve as a guide for future developments.</p>